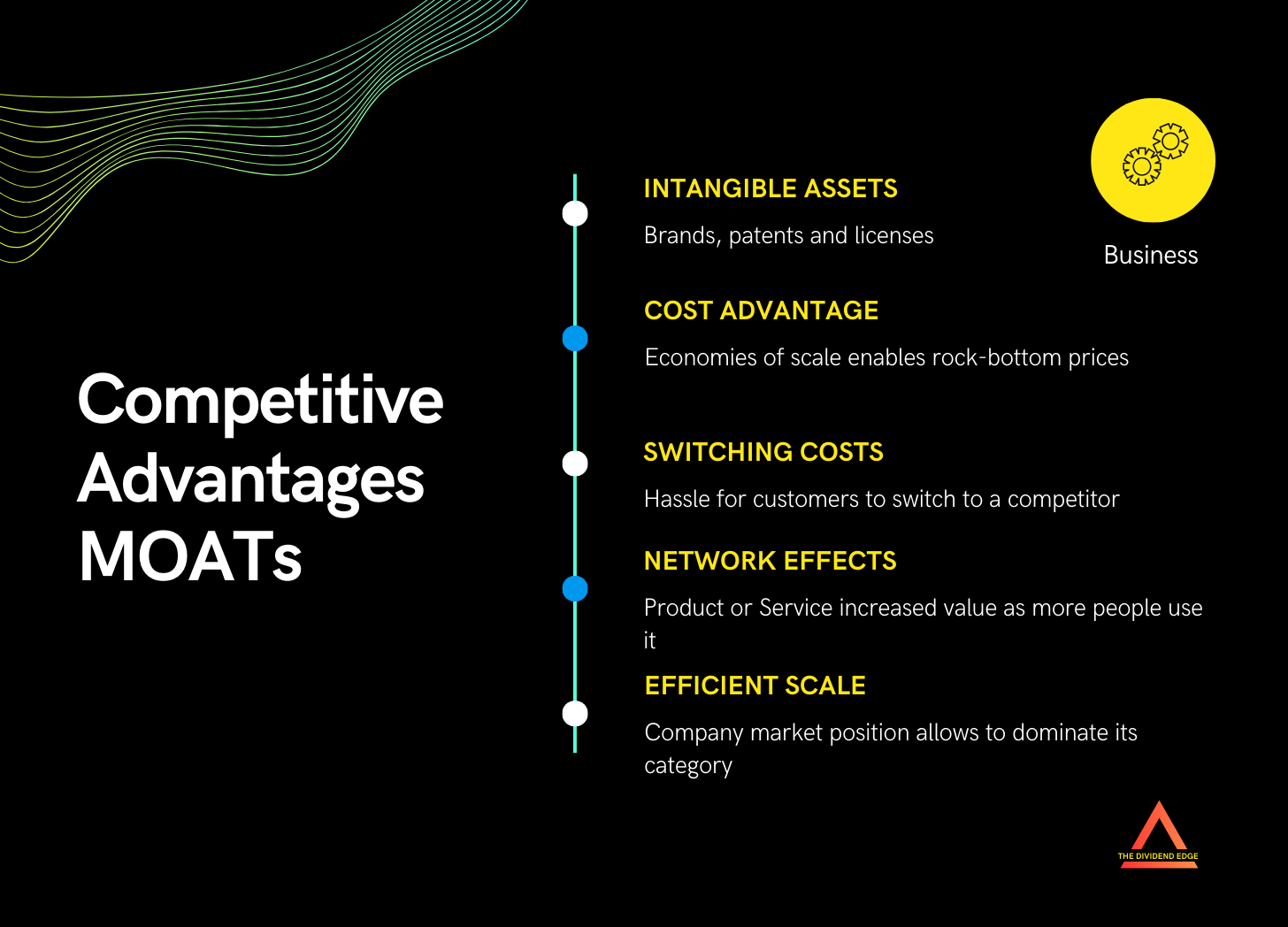

Competitive advantages

What make a business outstanding?

Hello fellow Dividenders!

We focus on outstanding companies that pay and consistently grow dividends, year after year.

The key to finding these outstanding companies? It's all about their competitive advantages, or "moats".

These moats are what allow a company to prosper, fend off the competition, and keep that dividend stream flowing steadily upwards. Let's dive into the key 5 moats types.

Intangible Assets

Think of brands, patents, and licenses. A prime example is Johnson & Johnson, with its globally recognized brands like Band-Aid and Tylenol. Their brand power is undeniable. Then there's Pfizer, a pharmaceutical heavyweight with a war chest of patents protecting their valuable drugs. These patents grant them exclusive rights to produce and sell those medications, a serious advantage. Other companies with moats based on intangible assets include Procter & Gamble, Coca-Cola and Nike.

Cost advantages

Walmart is a classic case. Their massive scale allows them to strong-arm suppliers and negotiate rock-bottom prices, which they then pass on to customers, making it tough for smaller retailers to compete. Another is Costco through their membership model and focus on selling a limited selection of items in bulk. This allows them to minimize operating costs. Other companies with this type of moat are Home Depot, UPS and McDonald's.

Switching Costs

These are the barriers that make it a real hassle for customers to switch to a competitor. Microsoft, with its widely adopted Office suite, is a great example. Once a business is fully integrated with Microsoft's ecosystem, migrating to a different platform is a logistical nightmare they are unlikely to attempt. Salesforce is another example, as well as other companies such as Adobe, Autodesk and Intuit.

Network Effects

Meta Platforms (formerly Facebook) is a prime example. The more users join their platforms, the more valuable they become to other users, creating a virtuous cycle. Visa and Mastercard operate global payment networks that similarly benefit from network effects. The more places that accept their cards, the more valuable they are to consumers, and vice-versa. Other companies that use this to their advantage include Amazon and Alphabet.

Efficient Scale

Think of companies that dominate a market where it simply wouldn't make sense for new competitors to enter. Union Pacific, a major railroad operator, benefits from this. Building a new railroad network to compete would be incredibly expensive and inefficient. Other companies with an efficient scale moat include Waste Management, American Tower and Equinix.

How do we spot these moats on a company's financial statements?

For intangible assets, look for a significant amount of "goodwill" on the balance sheet (though this can be tricky, as it can also arise from overpaying for acquisitions), but more reliably, look for consistently high gross margins, a sign of brand power.

Cost advantages are reflected in higher operating and profit margins compared to the industry average. Switching costs often show up as high customer retention rates and strong, predictable recurring revenue. You might also see a hefty amount of deferred revenue on the balance sheet. Network effects often result in rapid revenue growth, especially in the early stages. While for efficient scale, look for companies with stable returns on invested capital (ROIC), capital intensive (CAPEX 30% or higher of FCF) but with above normal gross and net margins and dominant market share within their niche.

The kicker: these moats often lead to Pricing Power.

A strong brand like Johnson & Johnson's can command a premium price. Pfizer, with its patented drugs, can charge more because they're the only ones legally allowed to sell them. Companies with high switching costs can often implement modest price hikes without much customer churn. Network effects make a product or service more valuable as it grows, justifying higher prices. And in an efficient scale situation, lack of competition gives a company significant leeway in setting prices. Companies with strong cost advantages can also decide to increase prices due to their superior cost structure.

Pricing power is a beautiful thing for investors because it translates into fatter profit margins, more predictable earnings, and, importantly, a greater ability to keep those dividends growing. So, when you're looking for those dividend growth champions, focus on companies with wide, deep moats. They're the ones that are built to last, that can weather economic storms, and that have the power to reward shareholders handsomely over the long haul. Do your due diligence, scrutinize those financial statements, and seek out those moats. They might just be the foundation of your portfolio's success for years to come.

Until next time,

The Dividend Edge